Loading content …

Heading for a Trend Reversal on the Financing Market

Despite the challenges caused by high rates of interest, there are first signs of a slight normalisation in the financing market. During the first quarter of 2024, the real estate financing volume of the member banks of the Association of German Mortgage Credit Banks (vdp) increased to 27.0 billion euros. The increase is mainly explained by intensified bank lending for the construction and acquisition of residential real estate. The real estate industry should not be expecting too much from the ECB’s interest rate decisions.

As expected, the European Central Bank (ECB) announced merely a minimal interest rate cut today (Thursday, 6 June).

The ECB has often been criticised for its notoriously reluctant interest rate policy. We believe the criticism is well deserved. That said, it should be remembered that the ECB is responsible for maintaining the price stability in all countries of the single currency area, where the inflation trend differs considerably from one country to the next. For example, the annual inflation rate in May 2024 equalled 2.4 percent in Germany and France but was significantly higher in countries like Croatia and Austria at 4.7 percent and 4.1 percent, respectively. These differences limit the ECB’s options for potential interest rate cuts because its mission is to bring the inflation down to a level of 2.0 percent in all of the eurozone member states if possible. Add to this that inflation in the services sector has been particularly stubborn, showing an inflation rate of 3.7 percent in April 2024. On the other hand, the impact of monetary policy decisions on markets is subject to serious delay. So, if the ECB always waits until a change in inflation trend has become a verifiable fact, any shift in interest rates will necessarily come too late.

Another aspect particularly important for the real estate industry: The interest rate decisions made by the ECB only concern short-term interest rates. Although these have become a major cost factor for property developments once more, long-term interest rates play a far greater role in pricing. Here, the ECB is planning to gradually roll back its activities, i. e. to reduce its balance sheet portfolio of non-current loans and securities. This could actually prompt an increase in long-term interest rates. However, the ECB has proceeded with great caution in the recent past. There are various reasons to assume that the pace of the interest-tightening moves will remain rather slow. This means that changes in long-term interest rates are most likely to come if the long-term inflation expectations were to experience another drastic shift.

Irrespective of the ECB’s actions, the figures for the first quarter of 2024 show that the situation on the real estate financing market has improved already. For one thing, the volume in residential mortgage loans increased by 7.1 percent to 17.8 billion euros in Q1 2024. Likewise, financing approvals for office real state increased by 19.6 percent over prior-year quarter. These developments show that financing deals that may have been impossible to place are now becoming marketable again and are picked up by lenders. At the same time, the need for market intelligence has stayed high, and financing decision keep taking a long time. Lenders remain cautious. And yet: There are manifest signs of an incipient, incremental normalisation.

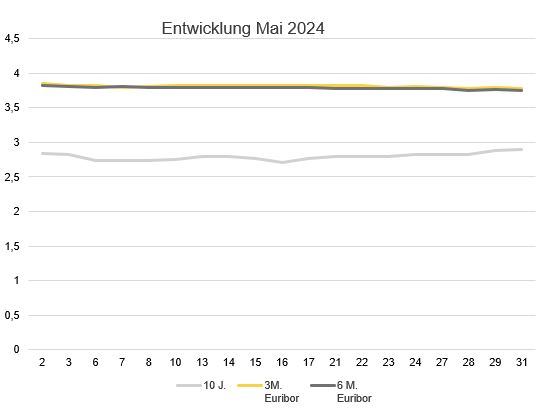

Interest

Short-term interest rates declined slightly in May, whereas long-term interest rates increased slightly. The 10-year interest rate swap equalled 2.84 percent at the start of May, and went up to 2.90 percent over the course of the month. The 3-month Euribor rose from 3.853 percent at the beginning of the month to 3.785 percent as May progressed. Analogously, the 6-month Euribor fell from 3.828 to 3.745 percent.

Outlook

The ECB remains cautious in its interest rate policy in order to ensure stable prices across the entire eurozone. There are currently no signs of an imminent change of the level of long-term interest rates. It is expected that prices could continue to soften during the second half of 2024, which would encourage transactions and refinancing arrangements. There is already an increase in marketable requests for funding, and lenders have started offering acceptable terms and conditions again. Despite persistent challenges, the market in general seems to be heading toward a gradual recovery.