Loading content …

Inflation and Real Estate Prices: Encouraging Signals but No Definite Trend Reversal Yet

We seem to have put the inflation issue behind us. In August, the rate dropped back below the magic threshold of 2.0 percent. However, a closer look suggests: It would be premature to close the book on the spectre of inflation. We also started getting a flurry of good news from the real estate market. But this, too, should be taken with a grain of salt. We have yet to see unambiguous evidence of a trend reversal.

The big news interrupting the summertime lull of 2024 was a report by the Federal Statistical Office that the inflation rate hit 1.9 percent in August and thus dropped below the magic mark of two percent. It prompted many in the media to announce the end of the inflation cycle, with some seeing it as an opportunity for the European Central Bank to lower its lending rates on 12 September. At present, the ECB’s key lending rate still stands at 4.25 percent. Since most forecasts see this interest level return to 3.5 percent by the end of 2024, with only three more monetary policy decision dates left this year, it seems reasonable to expect three interest rate cuts of 0.25 percent each.

But the ECB should ignore the expectations of Germany’s experts and capital market. After all, a closer look reveals that the inflation trend is not quite as rosy as August’s inflation rate of 1.9 percent would seem to suggest. It merely reflects a temporary development that is attributable to the typically wild fluctuations of energy prices. As early as September, the inflation could be well above 2.0 percent again. This is suggested by wage growth far beyond 2.0 percent, among other reasons. Wages increased by 5.4 percent in Germany during the second quarter, and by 5.1 percent across Europe during the first quarter. They are a major price driver, most notably in the services sector.

Moreover, the ECB does not take its cue from the inflation trend in Germany but from that of the European single currency area as a whole. In the latter context, it pays particular attention to the core inflation rate, which disregards the volatile prices for food and energy. In June, the eurozone’s core inflation rate stood at 2.9 percent, and it was still at 2.8 percent in July and August. Since the level was significantly above 3.0 percent during the first quarter, this represents admittedly a regressive trend compared to the preceding months. But this does not change the fact that the core inflation rate continues to top the central bank’s target benchmark, and significantly so. In fact, the core inflation rate is projected to average around 3.0 percent in 2024 and around 2.5 percent in 2025. Striking to note: The ECB itself is far more optimistic in its forecast: It anticipates 2.2 percent in 2025, while all of its predictions for 2026 and thereafter are near 2.0 percent. With this kind of outlook, the central bank has principally laid the ground for justifying further interest rate cuts.

But that is not the way we see things: In our opinion, it would still be too early to lower lending rates any further. Considering that a premature interest rate cut would do more harm to the real estate industry than a belated one, we hope that the ECB maintains its traditionally cautious monetary policy in September, too. The positive ramifications of exercising prudence manifest themselves in the performance of long-term interest rates: Since market players expect the inflation rate to come down eventually, long-term lending rates have continued to soften slowly, if steadily, this month.

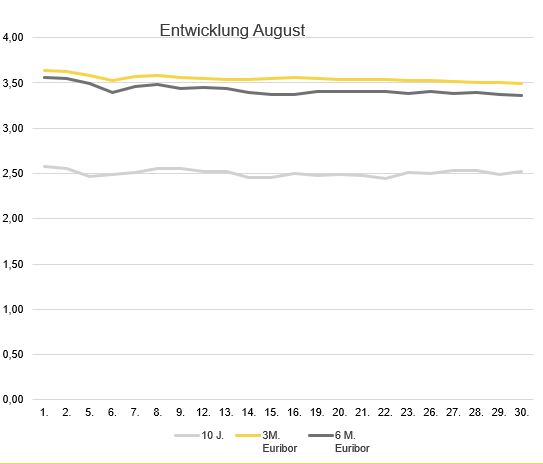

Interest Rate Development

Swap rates for ten-year interest rates dropped by a modest 26 basis points in August, from 2.58 percent down to 2.52 percent. Short-term interest rates were somewhat faster to decline. The six-month Euribor descended from 3.56 percent to 3.36 percent. The three-month Euribor fell from 3.63 percent to 3.49 percent.

Outlook

Sadly, there is no definitive evidence yet for a trend reversal in interest and inflation levels, even if they are heading in the right direction. A stream of good news has started coming from the real estate market itself. For instance, new bank lendings to private households and self-employed persons have reached the highest level in two years. This, however, is still well below the pre-crisis level. What is more, the trend has yet to spill over into commercial real estate financing.

When it comes to real estate pricing, the market presents a murkier picture than many market player would like to see: The price trend in most segments has not stabilised to a degree that would encourage broad-based price growth. On the whole, prices do not point to an unambiguous trend reversal yet. For what it’s worth, however, the latest figures released for the second quarter by the VDP Association of German Mortgage Credit Banks, for instance, indicate a sideways drift in many segments. We may not be out of the woods yet, but have perhaps put the worst of the crisis behind us.