Loading content …

Drop in Key Lending Rates Does Not Automatically Stimulate Real Estate Market

The EZB is moving through an interest rate cutting cycle. There have been five interest rate cuts so far and there may be another three before the end of 2025. We take a dim of the strategy because the inflation has not quite been overcome yet. Moreover—and this is not the first time we said so—lower key lending rates do not imply that ten-year interest rates, which are crucial for the real estate market, are falling at the same rate. On the contrary, they might actually rise.

On 30 January 2025, the European Central Bank (ECB) lowered its key lending rate for the fifth consecutive time. Although the ECB had not unambiguously announced the interest rate cut, it had been anticipated by the majority of market players. Just ahead of its monetary policy decision date, the central bank had stated that it expects the long-term inflation rate to hover around two percent. This would actually match the inflation target pursued. As a result of the key lending rate cut, loans to private individuals and entrepreneurs could become cheaper, and thereby cushion the economic slowdown.

However, the ECB’s monetary policy decision is not without risks. Inflation has not been curbed in the eurozone yet. In January 2025, the consumer inflation rate increased to 2.5 percent, up from 2.4 percent in December. This puts Germany slightly above the eurozone average. The inflationary momentum was driven most notably by the services sector. Here, the inflation rate currently stands at 3.9 percent.

Although the present rate of inflation still exceeds the target benchmark of two percent, and significantly so, the ECB has lowered its key lending rate again. The move could backfire – for two reasons: On the one hand, a change in key lending rates will generally take a year or two to impact the real economy. This means: The previous interest rate cuts have not even worked their way through to the real economy yet.

On the other hand, capital markets respond very quickly, unlike the real economy. By lowering its lending rates, the ECB continued to roll back its inflation-fighting measures. If market were to be hit by fears of resurgent inflation because of the ECB’s rate cuts, it could drive up long-term interest rates rather quickly. The danger is compounded by another development: The ECB is downscaling its portfolio of long-term bonds. Doing so tends to drive up yield rates as well, and long-term interest rates with them. However, the volumes at issue here are comparatively small, so that we need not worry about any major ramifications.

As we have repeatedly pointed out, the rate cut in and of itself does not seriously affect interest rates on ten-year financing arrangements, which are crucial for the real estate market. Interest rates for private construction finance, for example, remained largely stable in 2024. Following the second-to-last key interest rate cut by the central bank on 12 December 2024, the ten-year swap rate climbed from 2.22 to 2.6 percent within a short period of time. It probably represents but a snapshot and is unlikely to have been prompted mainly by the ECB policy decision. But the development shows that a key interest rate cut may coincide with a increase in long-term interest rates. In the medium term, the key interest rate cut will ease the cost burden for property developers and builders. That said, the relief is too insubstantial to be a factor in building decisions.

Interest Rate Development

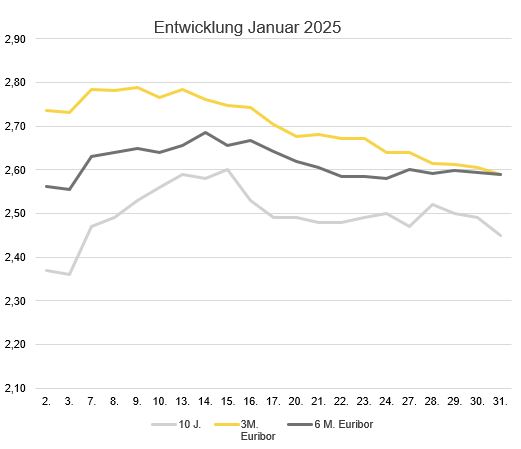

The three-month Euribor lost 0.15 basis points in January, falling from 2.74 to 2.59 percent. By contrast, the six-month Euribor went up slightly from 2.56 to 2.59 percent despite the key interest rate cut. Long-term interest rates ascended slightly faster. Continuing its trend, the ten-year swap rate rose from 2.37 percent at the beginning of January to 2.45 percent by month-end.

Outlook

The next monetary policy decision date is 6 March 2025. It is currently expected that the lending rate will be lowered by another 0.25 percent that day. Overall, a total of three or four interest rate cuts by 0.25 percentage points each have been predicted for 2025. Short-term interest rates, such as the three-month Euribor, are very likely to fall at the same pace. The trend in long-term interest rates, by contrast, is much harder to predict. The majority of experts anticipates a sideways movement. The trend in building finance rates is unlikely to trigger a significant impulse for the real estate economy. But that does not seem to be necessary anyway. It may be premature to assume that the economic downturn has ended and that real estate prices are bouncing back. For what it’s worth, however, we do know that lending volumes in real estate finance have slowly but steadily started to grow again in 2024. Let’s hope that the trend continues going forward.