Loading content …

Outlook for 2025: Between Geopolitical Chances and Hopes for Germany’s General Election

Several major geopolitical shifts are currently under way: Donald Trump was re-elected as President of the United States, and an end to the civil war in Syria appears to be in sight. But even more important for the real estate sector is another upcoming event – Germany’s general election on 23 February 2025. At this time, there is no telling whether the next governing coalition will be able to set the strong impulses that the German economy needs.

The coming year will probably usher in a series of major geopolitical changes. Donald Trump will return to the U.S. presidency while the war in Syria may finally draw to a close, and even Ukraine could see some material changes. By comparison, the ballot to elect the next German parliament seems almost like an afterthought.

But let’s start with the new man in the White House: Donald Trump will serve a second term as President of the United States, the world's largest economy and the most important export destination for German goods and services. It is hard to say at this time whether the tariffs he pledged will actually be introduced or whether they were mainly campaign bluster. Tariffs could, in any case, seriously hurt trade relations with Germany and cause further harm to the already ailing automotive industry, among other sectors. However, their initial effect would be an increase in inflation on either side of the Atlantic as a result of rising import costs, with the ramifications likely to be more keenly felt in the U.S. than in the EU. But at the same time, tariffs would impact the business cycle, which in turn would dampen inflation.

Meanwhile, a piece of good news appears to concern a conflict that has dragged on forever: The civil war in Syria is presumably winding down. At the face of it, this is a welcome piece of news, even though it is far from clear whether the next Syrian government will be less repressive than the previous one or indeed which way the country’s politics are heading. A sober weighing of possible consequences for Germany will, for the time being, suggest that Syrians living in Germany may be able to go back home, and the majority of them will probably need no prompting. If this came to pass, it would surely help to defuse the migration debate. It would also ease some of the strain that the migrant crisis caused. However, Germany could also suffer a migrant labour drain of about 200,000 workers. The bottom line is that the economic repercussions would probably be manageable.

The situation in Ukraine presents a very different picture. An end to the war is nowhere in sight. Trump announced cuts to the military aid for Ukraine, and plans to force the two belligerents to the negotiating table. We would not presume to predict the probability of any possible scenario. Regardless of how things evolve, it is safe to say that Germany will have to make a major effort to restore its defensive posture. However, the economic impulses thereby generated will not suffice to offset the adverse development in the automotive industry. Instead, chances are that increased defence spending will come at the expense of other important measures for which funds would otherwise have been earmarked in the federal budget.

That said, the outcome of the next general elections matters more to the German real estate industry than the momentous geopolitical upheavals. The Christian Democrats are unlikely to lose their current lead. Yet a coalition with the Liberals is hardly in the cards. According to the latest polls, the Christian Democrats may be lucky enough to win a narrow majority for a rerun of the unpopular coalition with the Social Democrats. Worse yet, it may be necessary to take the Greens aboard as well, so that the next government, like the incumbent one, will have to reconcile the very different agendas of three political parties. Implementing strong policy impulses of the sort the German economy—most notably the building industry—needs would remain as difficult as it is now.

Interest Rate Development

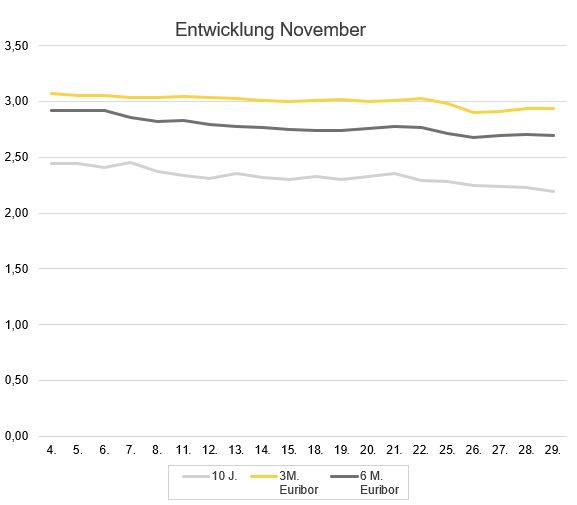

Both short-term and long-term interest rates declined in November. This was most conspicuously demonstrated by the performance of the ten-year swap rates, which dropped from 2.44 percent at the beginning of the month to 2.19 percent by its end. The six-month Euribor fell from 3.08 to 2.9 percent and the three-month Euribor from 2.92 to 2.70 percent.

Outlook

In line with the implementation of the “Basel IV” guidance, the capital adequacy requirements for banks will be further tightened as of the start of next year. It appears that Germany’s banks are well prepared for the regulatory change. This is visibly reflected in the latest edition of the BF.Quartalsbarometer, which shows that sentiment among lenders has continued to brighten, albeit on a low level. However, banks will reduce their overall lending volumes and reshuffle them to prioritise lower-risk loans. This does not necessarily imply that risky real estate developments are no longer financed. Banks and alternative financiers remain principally interested in healthy projects. Yet there is already growing evidence that both new financing arrangements and loan renewals will be thoroughly scrutinised, which can take up to 18 months, depending on the complexity.

The next German government will face diverse geopolitical developments as well as the acute problems of the automotive industry. Irrespective of its constituent parties, the governing coalition will also have to deal with the subject of affordable housing. But whatever the new government may look like, it will not be able to remedy the fundamental issues of the real estate sector. It is essentially the industry itself that will have to find workable solutions. For many companies, 2025 will be yet another tough year, and not all of them will stay afloat. But the modest improvements we witnessed over the past few months inspire hope for the gradual recovery of the markets.